In June, the price of the urea market, which shows the price of the shipment, is known to be low in inventory of most urea companies, and the car delivery strain, and the rate of urea in June is better than expected, and what is the report of the urea market in July?

First, in June, the focus on agricultural demand is a rebound.

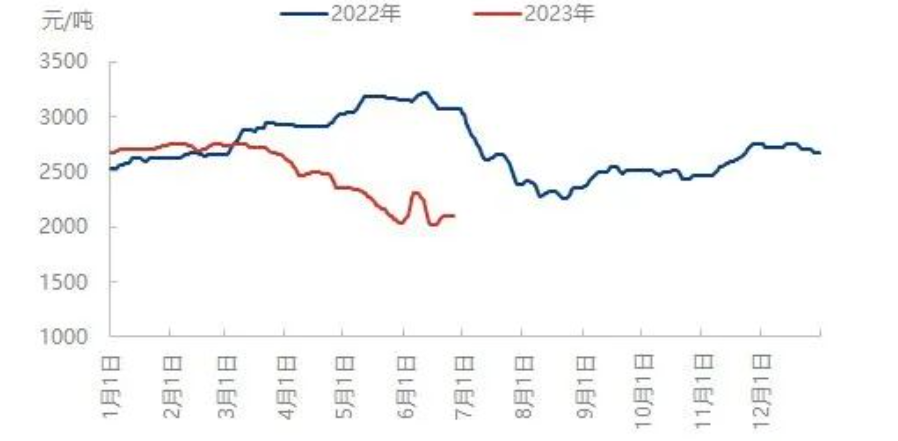

Domestic urea price trend contrast

In June, the domestic urea market fluctuated within the range, and small markets frequently appeared. In the early ten days, due to the concentrated demand in agriculture and the introduction of urea bidding news in India, urea prices rose sharply, and the local market rose by more than 200 yuan/ton in a week. Around the middle, the market gradually cooled down, on the one hand, the operation rate of compound fertilizer declined significantly, the procurement demand of agricultural wheat harvest stage weakened, urea daily high operation, the market continued to be bearish expectations, and the price turned downward after the lack of upward power. However, due to the superposition of industry and agriculture in the early stage, the inventory of urea enterprises fell sharply. When local agriculture continued to fill positions in the latter part of the year, some enterprises appeared tight shipments, and urea enterprises in Shandong, Henan and other places stopped short of failure, local supply and demand were tight, urea spot market was relatively strong, and local stability rose. Near the end of the month, the situation of local goods tight prices is more obvious, and prices in most regions are steadily rising.

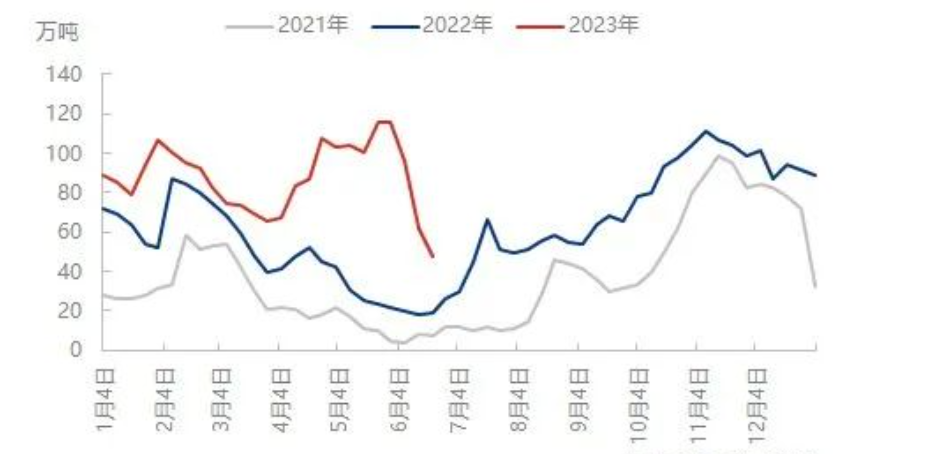

Domestic urea enterprises inventory comparison trend

The concentrated release of demand has promoted the rapid storage of urea enterprises, and the inventory of enterprises will further decline this week. According to the market, the current low inventory of most urea enterprises, and even some urea enterprise orders have been placed to the middle of July, and other parts of export orders are quietly appearing, short-term urea enterprise inventory pressure is not large. This provides a positive support for the continued urea market.

There are still big variables in July: the gap period is shortened and pushed back, and exports and other favorable conditions may still exist

June urea market performance is obviously better than expected, in addition with the end of June, the first half of the urea price trend is a foregone conclusion, from the price rise and fall point of view, as of June 27, Hebei small particles mainstream factory 2050 yuan/ton, compared with the beginning of the price fell 600 yuan/ton, compared with the same period last year down 1000 yuan/ton, urea fluctuation law, The risks of urea operations have been significantly reduced. Although in July, the traditional demand gap period, but the northern local agricultural demand or continue to early July, after the middle of the compound fertilizer operating rate or a rebound trend, but the plate industry in July still have operating rate is expected to decline, the overall downstream demand is expected to be in a stage difference, although the price has a correction trend, but also buried the possibility of the downstream to cover the low position. In addition, there are changes in exports, the recent export action is more frequent than the previous period, international prices have rebounded, and whether urea exports can follow the trend in the later period will also affect the urea market.

|

|

| Xuzhou, Jiangsu, China | |

| Phone/WhatsApp : + 86 19961957599 | |

|

Email : Kelley@mit-ivy.com http://www.mit-ivy.com

|

Post time: Jun-29-2023